The latest assessment of new capacity changes in the US electricity grid so far this year illustrates how quickly the massive decarbonisation shift is accelerating, both in the US and globally.

The inevitable rise of massive deployments of low cost wind and solar is clear, and solar deflation is set to re-emerge with module prices down a third year-to-date in 2023, a clear contrast to the higher energy price inflation driven by fossil fuel commodity manipulations globally.

Battery energy storage systems (BESS) are increasingly being prioritised over gas peakers for firming of low cost, intermittent renewables. And as deployment of firmed renewables accelerates, similarly momentum around coal power closures is building.

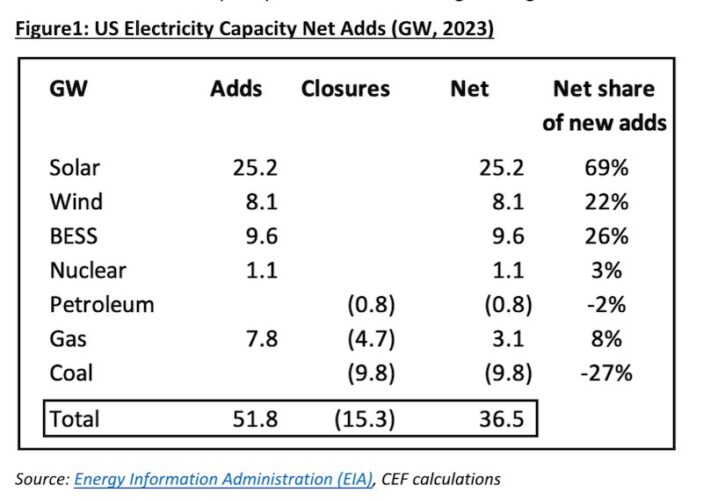

Almost 10 gigawatts (GW) of coal plants will close in the US in 2023 alone, 5% of the entire US coal fleet, as coal continues to plummet from the above 50% share it held as recently as 2008.

The Institute for Energy Economics and Financial Analysis (IEEFA) projects that the US is on track to close half its coal generation capacity by 2026, just 15 years after its peak.

US installations of utility scale solar are forecast by the Energy Information Administration (EIA) at 25.2GW in 2023 (excluding a record 5-6GW pa of rooftop solar), representing two-thirds of all net new capacity additions to the US grid – Figure 1.

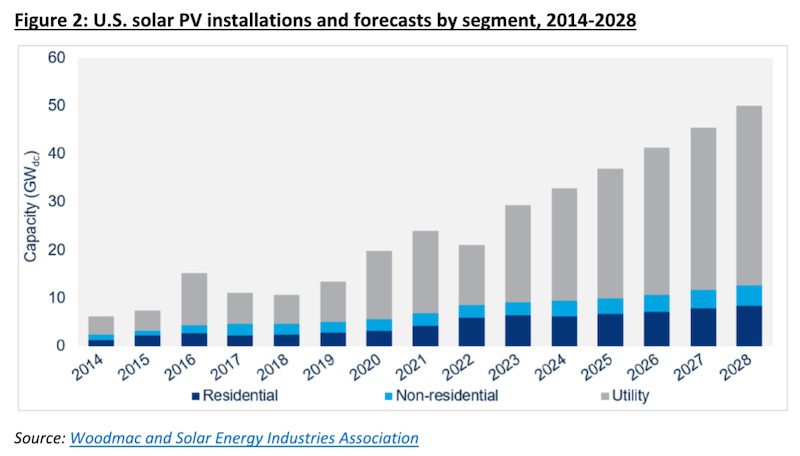

Woodmac forecasts total US solar installs will almost double to 50GW pa by 2028 (including rooftop), driven by the overwhelming economics of ongoing solar deflation and boosted by the US Inflation Reduction Act (IRA) – Figure 2.

Climate Energy Finance highlighted in our June 2023 China solar report our expectation that double digit solar cost deflation would resume in 2023, and continue through the coming decade.

Canadian Solar highlighted this month the 77% decline in polysilicon prices year-to-date in 2023, and the resulting 33% decline in Chinese export solar module prices in the same period, with this trend also evident in Europe. BNEF reports the world invested US$335bn in solar in the first half of 2023, +14% year-on-year.

The National Bureau of Statistics reports China installed a record 78GW of solar in the first six months, +154% y-o-y (some 8 times the rate of US solar installs).

For all the discussion of a mythical resurgence in nuclear globally by certain vested interests and lobbyists in Australia aiming to distract from and delay the transition towards renewables, the international experience demonstrates that nuclear is not a viable option here in Australia given the need for solutions this decade, not in 20 years time.

In the US, a single 1.1GW nuclear unit was finally added in July 2023 at Vogtle in Georgia. This is almost a decade behind schedule and US$17bn over budget, highlighted by Reuters as possibly the most expensive power plant ever built, bankrupting Westinghouse Electric.

It has delivered none of the so-called ‘modular’ design advantages spruiked by its proponents, with the massive cost to be borne by rate-payers for the next four to five decades.

Firming of renewables to ensure reliability of supply remains critical. The solar-induced ‘duck-curve’ is very clear already in the US, as it is in Australia.

As the US accelerates least-cost, zero emissions renewable energy infrastructure, it also leads the world in deployment of BESS.

Whilst China is leading the world in the deployment of pumped hydro storage (with a reported 89GW PHS currently under construction, adding 10GW pa), the US is expected to add a record 9.6GW of BESS in 2023, a near doubling relative to 2022.

At the same time, the US IRA is flooding the market with an unprecedented surge in battery manufacturing capacity in the US, Korea and globally, for both electric vehicle and BESS applications.

In Australia, the lobbying by fossil gas proponents is centred around perpetuating the myth of the transitional role of gas as a source of grid firming for renewables, while the US is illustrative of the massive change in investor intentions.

And while Australia’s multinational gas cartel has made fossil gas a very expensive domestic alternative, and gouged Australians by extracting above export parity prices for our own gas while banking superprofits, even the low cost US gas supply is seeing a record low 3.1GW of net new gas additions to the grid (7.8GW gross adds less 4.7GW of closures).

In Australia, it is noteworthy that gas peakers are uninvestable absent continued government subsidies, as EnergyAustralia’s 316MW Tallawarra B and Snow Hydro’s 660MW Kurri Kurri gas plants illustrate.

Federal energy and climate minister Chris Bowen’s Capacity Investment Scheme was very successfully launched in NSW in June 2023 in partnership with NSW energy and climate minister Penny Sharpe, lifting NSW’s firming tender from 380MW to 930MW of new BESS capacity.

In May 2023 RWE announced it would build a 50MW/400MWh world first longer duration BESS assisted by a NSW Long Term Energy Service Agreement (LTESA), co-located with the Limondale, NSW solar project.

That 9.8GW of US coal plants will close in 2023, 5% of the entire US coal fleet, illustrates the ongoing trend as coal continues to plummet from the above 50% share it held as recently as 2008, to an EIA estimate of just 16% share in 2023, and 15% in 2024.

In Australia, whilst coal lobbyists continue to push for a taxpayer bailout of the Eraring coal-fired power plant, the newly detailed decarbonisation plans for EnergyAustralia will see its emissions profile drop by 60% by 2028 with the closure of Yallourn lignite plant in Victoria, and the intention to shift its 1.4GW Mount Piper coal plant near Lithgow in NSW to a backup role more than a decade ahead of its scheduled retirement date.

The aim is to only run the plant around 20% of the time, and to schedule turning it off entirely for periods of time when higher penetration of renewables drives power prices to unviable rates. Variations of this strategy have been progressed in India and China to reflect the dual objectives of energy reliability and decarbonisation.

The electrification of everything theme is building strongly in Australia, with a world-leading move by Victorian energy and climate minister Lily D’Ambrosio bravely announcing the ban of new fossil gas connections from 2024.

Australia has run into significant headwinds in the development of new renewable energy resources at the speed and scale required to address the twin fossil fuel-driven climate and cost-of-living crises, not the least due to grid congestion and a community acceptance pushback.

However, CEF’s recent research shows there are more than enough utility-scale renewables proposals in the pipeline in NSW to offset capacity losses from the scheduled closures of Eraring and Vales Point coal power stations in 2025 and 2028 respectively, assuming approvals can be expedited.

There are also plentiful opportunities to accelerate distributed energy resources (DER) and to invest the $200-400 billion in public monies that would otherwise be spent in propping up Eraring into hastening the energy transition in the state.

The experience in Queensland shows there is likely to be significant existing spare capacity in the grid while the transmission buildout takes place.

Major stakeholders such as the Clean Energy Investor Group and peak clean energy industry bodies such as the Smart Energy Council are urging the NSW government to remain resolute and up its ambition.

Rather than backtracking on our ambitions, it is absolutely clear from the massive and growing cost of inaction on the climate crisis (including not only catastrophic extreme weather events, but also mounting economic costs such as unaffordability or unattainability of insurance) that we need to accelerate our combined efforts across Australia.

The time to act is now. Key to this is maintaining the planned schedule for coal closures as we redouble our efforts to transition the grid, a trend which is well established and accelerating globally in the US and elsewhere.

Tim Buckley is director of Climate Energy Finance