The real news in the NSW supply and reliability checkup is not the Eraring coal generator: It’s the changed role for EnergyCo and the recognition in the government’s response to the report that it needs to do a much better job of turning renewable energy zones into reality and getting stuff like HumeLink built.

It’s the success in getting new supply built and earning the requisite social license that is the main performance metric in my book. Second would be getting behind the meter storage to take off. Really, that’s all I care about. We need the new supply.

A government policy can either be for real or it can be lip service. It can be executed well, or it can be a bureaucratic nightmare.

In the end it comes down to the people entrusted with developing and executing the policy. New South Wales has a new government and a new energy minister. I view the government’s response to the reliability checkup as promising.

But so far it is just words.

The good news, on paper, is summarised in the following key headlines from the report:

- The NSW government will formally make the electricity system transition a strategic whole-of-government priority.

- EnergyCo will continue to lead the delivery of the REZs, but its structure, based on 1980s legislation, is not fit for purpose. The NSW government will move quickly to ensure EnergyCo has an appropriate focus ….

- As EnergyCo focuses on infrastructure and project planning and delivery, the energy, climate change and sustainability group within the office of energy and climate change – which will be part of the new Department of Climate Change, Energy, the Environment and Water (the Department) – will prioritise its responsibility for the overarching governance forums and the mechanisms under the Roadmap to enable the transition of the electricity system.

- Communities that host electricity infrastructure need genuine engagement and to share in the benefits of the energy transition.

Some of the more detailed and accepted recommendations include:

– That the Roadmap Intergovernmental Steering Committee (RISC) develops a whole-of-government plan for addressing community and workforce infrastructure needs and investments in the construction phase of the Central West Orana (CWO) Zone. That a transport and logistics plan also be developed by RISC for CWO.

– That EnergyCo establish high-profile offices in the REZs and look to increase local recruitment. (When AGL was building wind farms in South Australia 15-20 years ago there were local offices. There wasn’t that much drama).

– That the funding agreement between DPE and EnergyCo for faster planning approvals in REZs be expanded, and a coordinated approach taken to cumulative impacts and biodiversity assessments.

– That funding and resourcing of the Energy and Resources team in the Department of Planning and Environment (DPE) be increased.

ITK (that’s me) free suggestions (worth what they cost)

One thing governments are never short of is advice. It’s more or less the same for anything that the public has an interest in. Sports coaches get lots of free advice as well.

As an investment banking senior research analyst for many years I learned that the trick is working out what is noise and what is signal and for the signal how much weight to give it.

Anyhow…

Firstly, the NSW government and EnergyCo should use the regional community networks that already exist. I am primarily thinking of councils and shire councils. For instance, does Transgrid pay rates on easements? I don’t know.

Councils are often starved of cash but they don’t directly benefit from any development in their region. It’s not just Councils though, there are Chambers of Commerce, various clubs and associations.

Councils are a special case as they have revenue, expenses and formal responsibilities. They probably deserve a REZ and statewide “whats in it for councils” policy, but also bespoke consideration.

Councils have employees tasked with growing the region but additionally council members can be influential. Other networks within the region can be approached via members or by “outsiders”. Finding an insider is important.

Despite the noise there is clearly lots of support for wind and solar ,and therefore for the transmission that connects it all. The economic benefits are very real, not just to individuals but to the regions. Benefits don’t go unnoticed. You can’t simply buy social license but you can earn it and show that the benefits outweigh the costs.

Second: Regional constituencies that are outside of a REZ also need to see what’s in it for them. Humelink and Snowy region stakeholders are an obvious group.

I speak as someone that, if I squint, can see transmission lines from my office window and I live in a suburb covered with overhead distribution wires, a suburb where a 10 minute storm knocked down half the lines in the suburb and we were in blackout for 100 hours.

I note that you can run livestock under transmission and, subject to machinery size, you can crop around transmission. Complaints about existing transmission lines are in fact few and far between, or they were.

Every landowner that objects to transmission likely has overhead power wires going to their house. My point is, as bad as the visual impact is, within reason that is all it is at least outside of a national park.

They may have an impact on overhead fire fighting, although even a crop duster isn’t that much lower than a transmission height from my experience.

Third: Even if you can demonstrate rational value, the fact is people aren’t rational but behave in predictably irrational ways. (See Behavioural finance or eg “thinking fast and slow”.)

Fourth: As someone pointed out to me, there already exists a planning mechanism within NSW that could be adapted to REZs, this is the Special Activity Precinct.

Special Activity Precincts [SAPs]

Ironically these precincts came into use as part of the $4.2 billion Snowy Hydro legacy fund setup following the sale of NSW government’s interest in Snowy to the Feds. SAPs exist at Moree, Narrabri, Parkes, Wagga and the Snowy Mountains.

SAPs feature a precinct wide planning framework and may include:

- Government led studies

- Fast track planning

- Govt led development

- Infrastructure development

SAPs may or may not be suitable for a REZ. To my mind it doesn’t matter so much about the actual framework as the quality of the implementation.

A good determined leader with a decent team will make any structure work.

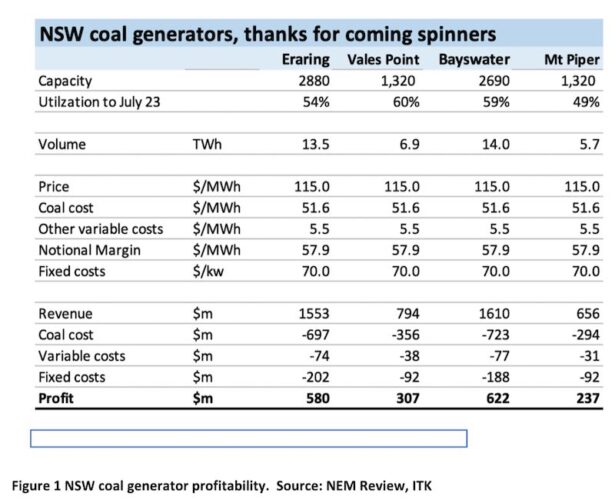

Eraring is profitable and a distraction – I’ll be trying to forget it

The outlook for Eraring is complex, but other than Origin and its employees we shouldn’t really care. My view is it will most likely stay open until say 2027/28 whether the government wants it to or not. I say that because:

1. It’s significantly profitable right now and would continue to be profitable, even allowing for 1 or 2 units to close in 2025. Closing some units will in fact prolong the life of the ash dam. Running it harder will fill the dam faster, shortening the life.

2. Origin is one of the two largest retailers of electricity in Australia. Management have publicly announced nothing in regard to post closure supply to this large retail base. That is, no new PPAs, no developments. Batteries don’t count, as they are net consumers.

But – and this is a big but – there will likely be a hedge and other contracts book of billions of dollars extending out to 2026 and possibly beyond. That’s the complexity of trying to negotiate with the company, even leaving aside the Brookfield overlay.

The government won’t know Origin’s contract book. Origin must take a view on their own supply one way or another and have enough to meet their contracted demand.

Origin has the largest commercial book in the country, ignoring AGL’s aluminium supply contracts. It has to take a view up to two years ahead about how much supply is coming from Eraring. Breaking any swap contracts will be expensive. Options and other hedge products might need to be closed out.

3. Any change in Eraring’s life will have to get a sign off from Brookfield.

A rough estimate of the profits of NSW coal generations, using a rough average of the baseload forward prices 2023-2026 is:

Estimates of new supply across the NEM using AEMO data

Here’s a table of AEMO’s estimates of new generation across the NEM. I’ve removed most of the commissioning generation from AEMO’s numbers as it’s mostly already operating at good levels of capacity.

In looking at the back of the envelope calculation for Eraring purposes I’ve removed NSW “likely” wind. For example, Uungula wind farm has already been held by Andrew Forrest at the starting gate for more than six months.

We still expect a notice to proceed this year but Forrest entities clearly have taken some time to sort stuff out. Forrest is entirely unproven as a wind developer and NSW and Queensland stakeholders aren’t the same as Western Australia.

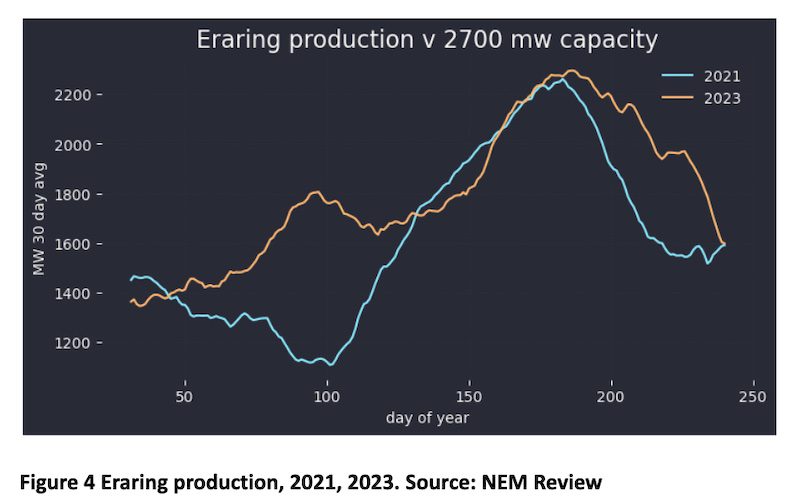

Bayswater has taken over Liddell’s output as expected

The following two figures compare Bayswater and Eraring output in the year to date with what they were doing two years ago. I ignore 2022, as coal constraints mean that just confuses the picture. Bayswater has lifted Winter production sharply to replace Liddell.

Eraring peak has barely changed.

Both Bayswater and Eraring have shown impressive ability to ramp during the last few months. On an average day they increase from not much over 1400-1500MW to 2500MW.

More solar will, of course, increase the ramping requirement, but this ignores the market response. We can be confident that storage will end up taking advantage of surplus midday power.

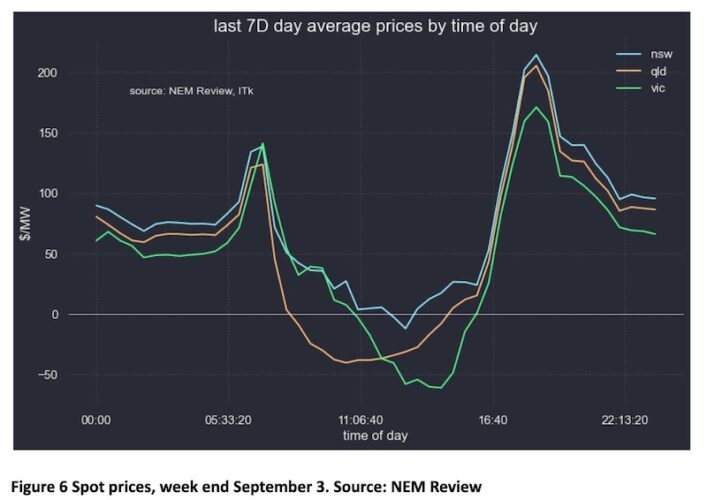

Spring sends midday prices consistently negative

Moving into Spring demand and electricity prices are soft. This can be seen from time of day prices in the major states over the past few days.

Prices in Queensland and Victoria are, these days, routinely negative in Spring. This is partly because of the seasonal uptick in solar production but also the lower cooling loads pushing demand down. That’s partly offset by an even larger than usual seasonal reduction in wind output.

And this in turn means that overall VRE output is barely above last year.

The extra supply in Queensland means that, at this time of the year, there is power to export all day including dinner time.

This pushes NSW into a surplus in the middle of the day and peculiarities in the transmission system mean that, even though power in NSW is more expensive in the middle of the day than in Victoria, nevertheless NSW power flows south to Victoria.