The DNA of BlueScope Steel, Australia’s biggest steel producer and a top global manufacturer of coated steel products, is in the Illawarra region, centred around the Port Kembla Steelworks.

While its future looked grim a decade ago, with the sector nearly lost to this community, BlueScope has roared back into rude financial health. With revenue comes the imperative for responsible investment to align strategically with the greater good of the climate and community, and that lays the forward-looking foundation for future economic opportunity.

BlueScope acknowledges that a “global green revolution” is one of the key drivers of demand for steel, which underpins the transition to renewable energy as electricity infrastructure (wind, solar and transmission).

Together with inputs such as critical minerals, it is a key enabler for our accelerating clean energy future. And its importance is elevated by the current geopolitical instability driving the need for enhanced supply chain security, and key trends such as China’s massively escalating renewables build-out on its path to decarbonisation.

According to Bluescope, “Demand for steel, coupled with industry shifts towards greater engagement… and standards setting, underpins our industry’s response to climate change”.

It is curious, then, that Bluescope Australia is really lagging, in contrast to its now dominant US position, where BlueScope continues to step up its aggressive investing as a leader in steel sector decarbonisation in terms of electric arc furnaces fed by its increasingly inhouse steel scrap recycling capacity.

It’s not for lack of capital. BlueScope reported a $3.79bn underlying EBIT result for FY2022, more than double FY2021, generating a 41.6% pretax return on invested capital, notwithstanding slightly lower overall volumes.

Reporting $1.71bn free cashflow, BlueScope exited FY2022 with a $367m net cash position, underpinning a high dividend payout and a further share buyback of up to $500m in FY2023, after completing a $638m buyback in FY2022.

In contrast to the steady state held in Australia, BlueScope has been expanding rapidly in the US, investing 100% of the $A2.1bn of recent growth investments, spread across four initiatives in lower emissions and value-adding assets detailed below.

In Australia, BlueScope has now proposed to sink $800 million to $1 billion into a reline of currently decommissioned blast furnace #6 at Port Kembla Steelworks.

Largely replicating now out-dated blast furnace technology in steelmaking that is hugely carbon intensive and entirely inconsistent with the science based target initiative (SBTi), with steelmaking releasing more than 3 billion tonnes of carbon annually.

This plan would entrench a legacy, high carbon emissions technology in the heart of Australian steelmaking for decades to come, just as we stand on the brink of an existential climate challenge coupled with building momentum for positive change.

This decision by BlueScope also fails to capitalise on emerging break-through clean energy technology alternatives being invested in by steel sector leaders around the globe: SSAB targets full decarbonisation of steel by 2026 via HYBRIT; Boston Metal; Kobe Steel Japan’s Midrex DRI in Canada with Rio Tinto; thyssenkrupp’s German and ArcelorMittal’s France DRI-EAF; FMG’s 67% magnetite iron ore at Iron Bridge; and Calix’s ZESTY.

Backed by its considerable financial strength and new Australian political NSW and federal government consensus on ambitious climate action, there is an enormous opportunity for BlueScope to lead steel sector decarbonisation and to secure its longevity and viability in ensuring its social licence to operate here in Australia, as it is doing in the US.

Currently, the #6 blast furnace reline project is undergoing a feasibility study to provide capacity for the replacement of the existing operations at the near-end of life #5 blast furnace.

BlueScope talks up the proposed $800m-plus investment as providing a possible bridge to potential so-called ‘breakthrough lower emissions steelmaking technologies, once technically and commercially viable’.

However, to CEF this is mostly greenwash and spin, a bridge to nowhere on the decarbonisation path, given it locks in continued high emissions for many decades to come.

BlueScope references some decarbonisation pilots for Australia: trialing biomass-coal blending for injection into the blast furnace; assessing a hydrogen DRI smelter concept for future iron supply at Port Kembla with Rio Tinto; and a 10MW pilot PEM hydrogen electrolyser / hydrogen refueling station feasibility study.

On the last idea, a tiny August 2022 footnote in the investor presentation says that while still a support partner, Shell is no longer leading on this proposal.

In FY2022 BlueScope also made an initial investment in Spectainer and Hysata, a University of Wollongong start-up focussed on developing a new more efficient hydrogen electrolyser cell.

However, BlueScope’s CEO has been assiduous in signalling publicly that change will not come to Australia’s leading steel firm, at least not this decade – the critical timeframe for accelerated progress on decarbonisation if we are to limit warming to 1.5°C.

Notably – and disappointingly – the Australian blast furnace reline investment represents half of the group’s total $1.9bn of future investment priorities, while proposed climate investments over the coming five years total just $150m or 8% of this total proposed spend.

This scenario does nothing to inspire confidence in the Bluescope board and CEO’s commitment to addressing the climate emergency in their country of domicile, despite their biggest problem being how to disperse the massive free cashflow gushing from their exceptionally high emissions Australian business.

It is also at odds with the pledge by 550 leading financial institutions in the Glasgow Financial Alliance for Net Zero (GFANZ), now representing a collective US$150 trillion of assets under management (AuM) to reduce their financed emissions in alignment with SBTi and a 1.5°C trajectory.

Credible transition plans for NZE are increasingly becoming a mandatory prerequisite for global investors’ continued support, and an increasingly central component of corporates’ social licence to operate, which is coming into sharper focus as ESG concerns and transparency in reporting rise to the top of the social, regulatory and financial agenda.

We note that in just two years the Global Net Zero Asset Managers Alliance has rapidly expanded to reach A$101 trillion of AuM (part of the GFANZ).

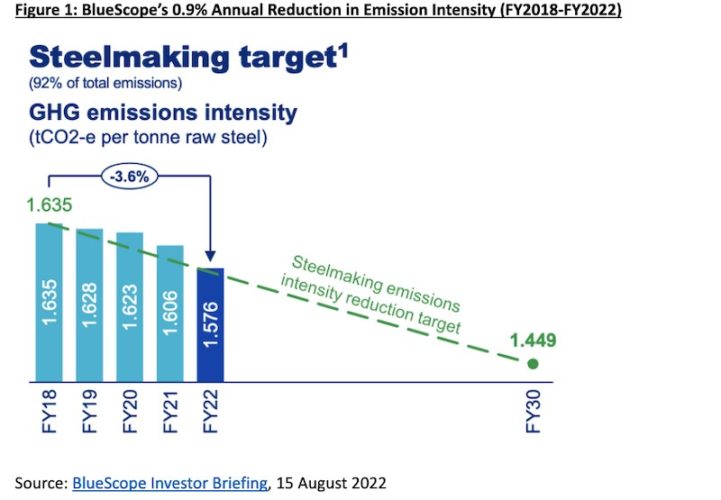

The issues outlined above are reflected in Bluescope’s underperformance on climate targets. Its reporting relies entirely on an unsubstantiated target for Net Zero Emissions by 2050, which would imply an average 3.5% annual reduction over the next 28 years.

However, the current board and CEO are committed only to an annual run-rate of less than one-third of this over the coming decade, with a stated interim 2030 target to reduce emissions by 12%, from a 2018 base. This is just a 1.0% annual emissions reduction.

Noting the carefully selected Y-axis is used to reference the 3.6% total progress in steelmaking emissions intensity over FY2018-FY2022 (Figure 1), a run-rate of an exceptionally pedestrian 0.9% pa. At 7% of BlueScope’s total, non-steel making emissions intensity is down 3.7% in the same period, again a pedestrian 0.9% pa, a third of the run-rate targeted for 30% reduction by 2030. BlueScope’s reporting under the Taskforce for Climate Related Disclosures (TCFD) is important, but a distraction until remotely SBTi aligned.

We note that back in July 2018 BlueScope signed at the time an innovative 7 year power purchase agreement for the equivalent of 88MW offtake from the Finley Solar Farm to supply 20% of BlueScope’s Australian electricity needs.

Whereas many Australian corporate leaders have subsequently signed on to target 100% renewables via RE100, in Australia BlueScope has been silent, beyond soaking up ARENA subsidies.

While BlueScope US now primarily utilises scrap steel, in Australia this hasn’t progressed beyond a possible pre-feasibility study. At a time that fossil fuel price hyper-inflation is fundamentally challenging business as usual globally, it is bizarre that the firm’s 2022 climate report still references delays in material action till next decade, more reflective of Dr Michael Mann’s inactivist tactics.

On the positive side, in the US, BlueScope is continuing an aggressive expansion strategy into low emissions steel assets. Despite a weaker second half, FY2022 EBIT from North America almost trebled to $2.0bn, a 60% higher contribution than the Australian steel business.

BlueScope generated 54% of FY2022 gross profits from North America. Tellingly, 100% of BlueScope’s A$2.1bn of recent growth investments were in North America. This reflected four new US investments:

- The US$770m ($1.0bn) North Star steel making expansion construction of a new EAF and Ladle Metallurgy Furnace (LMF) which is now substantially complete; commencing 18 month ramp up;

- Evaluating a further $100m North Star US hot strip mill debottlenecking project;

- Establishing BlueScope Recycling US with the acquisition of MetalX ferrous recycling business in December 2021 for $287m to provide surety of supply for a growing portion of NorthStar feedstock, with a further US$80m acquisition of an additional scrap processing site in Ohio in August 2022; and

- Acquiring 900ktpa painting capacity by acquiring Coil Coatings for $717m, providing vertical integration of a national US coil painting platform.

BlueScope is a powerful player in the Australian, NZ and US steel sectors and in the strongest financial position it has ever been in. We note the massive ongoing investment in expansion of increasingly vertically integrated modern lower emissions EAF steel operations in the US.

The looming board decision to undertake a massive $1bn BF#6 investment locking in reliance on high emissions antiquated blast furnace operations at Port Kembla Australia sits in stark contrast to the low emissions leadership BlueScope has shown in the US.

We note BlueScope’s overall target of a 1% annual reduction in emissions this decade sits at less than a third of the run-rate needed to reach net zero emissions by 2050, a target announced by the firm in January 2022.

Australia is perfectly positioned to be a renewable energy and future facing mining superpower, helping our key trade partners deliver on their key decarbonisation objectives.

Absent a clear price signal on all carbon emissions in Australia, we would call on BlueScope to think out-of-the-box about how a public-private alternative approach could serve Australia best.

This is particularly important in light of the strategic nature of the Albanese government’s ambitious but largely open-ended new $15bn National Reconstruction Fund and ambitious 82% Renewables by 2030 target, supported by the $20bn Rewiring the Nation fund.

Financial avoided carbon emissions options that were strategically impossible even a year ago should now be brainstormed.

It is time for a dramatic position reset so BlueScope plays a constructive leadership role, aligned with our government the way the Swedish, German and Japanese steel industries are working in partnership with their governments to bridge the emissions capex finance gap, as modelled by Agora of Germany. Far better this be done in-house than have it imposed down the track by investor dissatisfaction.

Tim Buckley is director of Climate Energy Finance