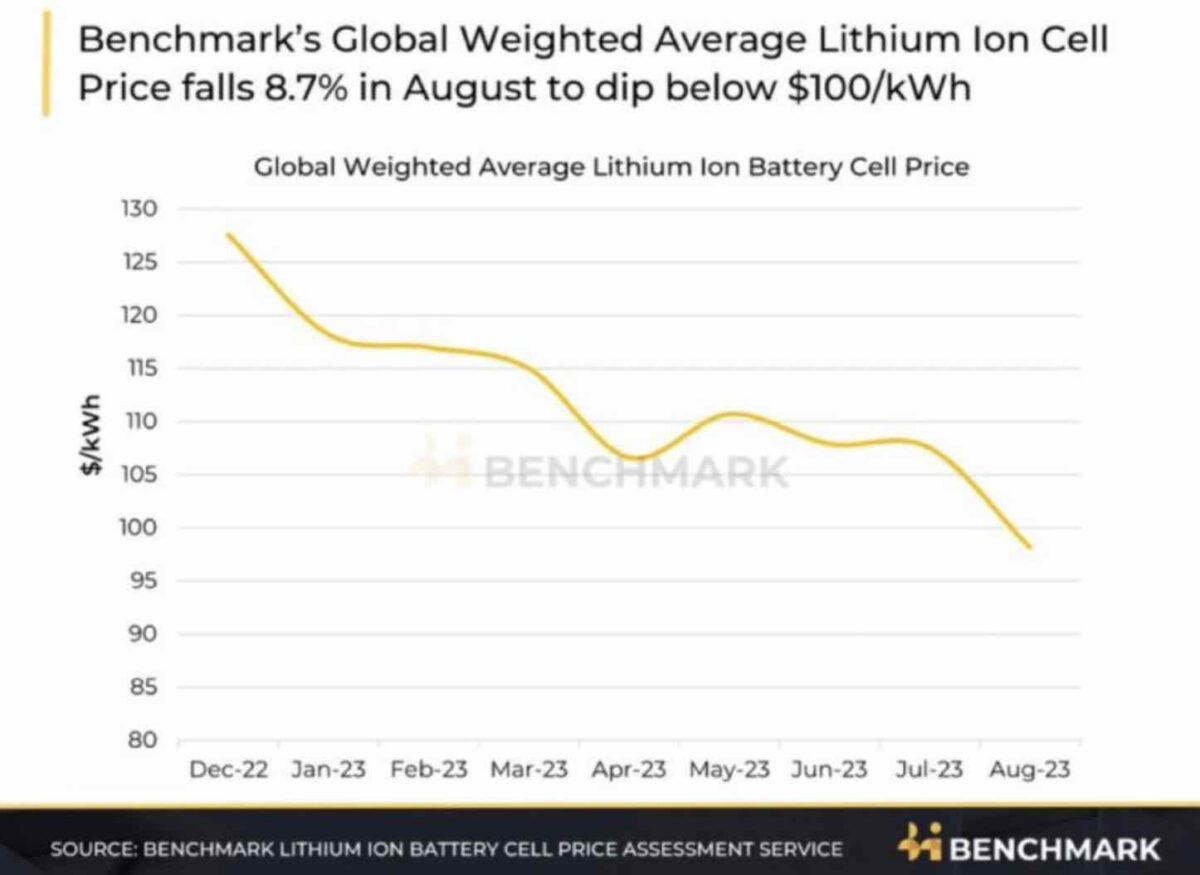

The price of battery cells has plunged in the last month, taking it below a key benchmark for the first time in two years, and close to the “tipping point” where the price of battery-powered EVs can match that of internal combustion engine cars.

According to leading analysts Benchmark Lithium, the global weighted average price of lithium ion battery cells fell 8.7 per cent in August, taking it below the $US100/kWh mark for the first time since August, 2021.

It is now priced at $98.2/kWh, a 33 per cent drop from the recent high in March last year of $US146.4/kWh, and is the result of a drop in key commodity prices, including lithium, nickel and cobalt.

Importantly, it is now not far from the $US80/kWh cell price that is crucial to delivering a $US100/kWh battery pack – the level that is considered a tipping point because it will allow EV makers to build electric cars that cost the same as petrol and diesel alternatives.

“The energy and transport revolution continues!” said Gerard Reid, a leading energy analyst and head of Alexa Capital. Reid said the price of lithium battery cells have fallen 80 per cent in a decade, and will continue to fall as they deliver better performance.

“That is why the death of the internal combustion engine is near,” Reid wrote on LinkedIn.

It is also good news for stationary battery modules used to soak up solar and provide storage in electricity grids dominated by renewables, and follows on from news that solar module prices have also plunged to record lows – reversing the price gains experienced in the last two years as a result of Covid and the war in Ukraine.

Benchmark Lithium says prices for most raw materials used for cell manufacturing have fallen significantly.

“For electric vehicles to reach price parity with internal combustion engine vehicles, battery pack prices need to reach $100/kWh, not accounting for subsidies. This corresponds to a cell price of around $80/kWh,” Benchmark analyst Evan Hartley wrote.

“Decreasing cell prices could allow OEMs to sell mass market EVs at comparable prices to ICE vehicles, with the same margin, improving the attractiveness of the EV transition for both consumers and automakers.”

According to Hartley, falling prices of battery metals and graphite have followed through into falling cathode and anode prices. Benchmark says its Cathode and Anode indices have fallen 41.9 per cent and 17.6 per cent so far this year, respectively.

On top of this, lithium prices have more than halved since the start of 2023 with Benchmark’s Lithium Carbonate Price Index dropping 52 per cent since the start of the year and the Lithium Hydroxide Price Index dropping 58 per cent.

Cobalt sulphate prices are also at their lowest level in the China market, and nickel prices have also dropped 25 per cent so far this year.

Hartley notes that prices of modelled prismatic NCM811 cells have dropped even further in China to a low of $US82.6/kWh, lower than $US85.7/kWh price for an equivalent LFP cell, and are close to the $US80/kWh price point needed to reach a $uS100/kWh pack price.

As in the solar market, this has consequences for battery makers who are not in China, unless they can achieve the same price reductions.