Transmission, supply chain, GPS are not the big issues they are often portrayed to be. Willingness to commit to investment is the big issue.

Price signals are also unambiguously positive, at least in New South Wales and Queensland and even a renewable developer can work out prices in Victoria will rise post after the closure of the Yallourn power station.

Yet over the past year we’ve all had to stand around and hear a long list of complaints from wind and solar developers. No transmission, supply chain, costs, GPS, uncertainty (God forbid that returns are not guaranteed).

The only thing anyone talks about is batteries, even though batteries are net consumers of energy.

The groups that have most disappointed me are the big renewable developers: Iberdrola, CWP (or whatever it’s called these days), Tilt and their ilk.

These guys don’t have the legitimacy of running coal generators to maximise end-of-life cash flows; they have large balance sheets and are completely capable of taking on some risk should they choose to do so.

Then, of course, there are the gentailers. At least their lack of commitment is normal. I laugh to see 70% of shareholders that voted in favour of the Origin scheme but now have to put up with a company that remains neither fish nor fowl and where uncertainty remains the order of day.

Australian Super’s “we’ll save ya” attitude, and ‘why don’t you buy some Santos or Woodside?’ comes really as no surprise.

For sure they are big and prove that size does matter. Poor old EnergyAustralia must wonder how Brookfield can talk to AGL and Origin, while it and its owner CLP are left as wallflowers, continuously passed over, despite showing all the leg they can get away with.

As usual, and I speak as someone who passionately believes in markets, it’s government, and in this case the Queensland government, that has stepped into the breach.

Nevertheless, the point of this note is to observe that:

- Transmission will be available in NSW from 2026 and plenty by 2028. It takes that long to build new wind farms, so these guys should be committing now.

- Supply chain issues, at least in terms of wind turbines, are not such a big issue. If you order a turbine from Vestas you can get it at the same euro price as last year. You can possibly get a Goldwind turbine for less than last year.

- Price signals remain strong and there is even more financial support.

- AEMO is, from what I can see, increasingly ready to rock and roll.

I guess it’s still legitimate to say that Humelink is not certain and the Orana contract has not actually been announced, but as Irving Fisher so poetically observed in the preface to Theory of Interest, “coming events cast their shadows before.” If I can see the transmission is coming with my fading eyesight, it must be crystal clear to renewable developers.

Two big events left this year

Results from AEMO Services’ second tender for renewable energy in NSW are expected to be released in the next couple of weeks. That should cover around 1GW of projects; a drop in the ocean but still very welcome news. Hopefully at least some new wind.

Energyco (AEMO Services’ partner in NSW) will also release a year-end update on Monday 11 December. It would not surprise me to find that the Orana transmission contract is also announced then.

Then, of course, the first draft of the 2024 ISP will also be released in the next couple of weeks. Although ostensibly a transmission planning exercise, the reality is that the 2022 ISP was the document that convinced stakeholders that we all, in reality, expected a decarbonised NEM – and sooner rather than later. Not so much price discovery as belief discovery.

In any event the ISP 2024 will embody state government policies such as Victoria’s offshore wind target, misguided as it may be, the Queensland plan, misguided though Borumba may be, and changes to the NSW outlook, including delays to Snowy 2. Personally, I could not give a rat’s about the delay to Snowy 2 or its cost. For me the world has moved on. Still, lets leave ISP 2024 until it’s released. Speculation is pointless.

Transmission outlook is improving

For years commentators have focused on transmission as the key enabler of a strong renewable electricity system. The earliest article I wrote about this here at Reneweconomy was on July 5, 2017: “Transmission we need to start building now”.

That was only a year after I left UBS. At that time the then AEMC chair, John Pierce oversaw a rigid approach embodied in the logical and seemingly rational – but ultimately utterly misguided – view of new transmission embedded in the RIT-T test.

It was clear, even then, using the best practice Texas example, it would take seven years to build new transmission, just as it was clear even then that the existing transmission network in the NEM would likely be in the wrong place for wind and solar. However, at that time it wasn’t clear just how congested the existing network actually was.

Despite the blackout in South Australia, by 2023 the only new transmission link actually being built other than some minor augmentations in the QLD-NSW link is the SA-NSW link – and that’s not due for completion until 2026. Indeed, building new transmission has taken every bit as long as feared back in 2017.

During this period, stoked by rabble rousers, fear and doubt (FUD) about the ability of Australia to build something as simple as some wires and poles has grown and grown.

Transmission and wind farms are now portrayed as ruining the Australian way of life, a source of endless depression and creating environmental destruction.

My view of reality is that renewable energy and the associated transmission will preserve the Australian way of life, bring more prosperity to regional Australia, and is the best thing that can be done to preserve the environment and will lead to lower and more certain electricity prices. Colour me a hippy.

Today a wide range of “experts” and advisors contend that the lack of access to transmission is the No. 1 problem preventing new renewable energy projects from starting.

Personally, I’m not fully convinced that transmission is necessarily holding back projects right now. I think wind and solar developers lack a willingness to commit, perhaps hoping to move the dial in their favour.

For instance, the 400MW Uunguala wind farm in northern NSW could have started construction 12 months ago but Twiggy Forrest seems too busy posturing on the world stage to sign the contract.

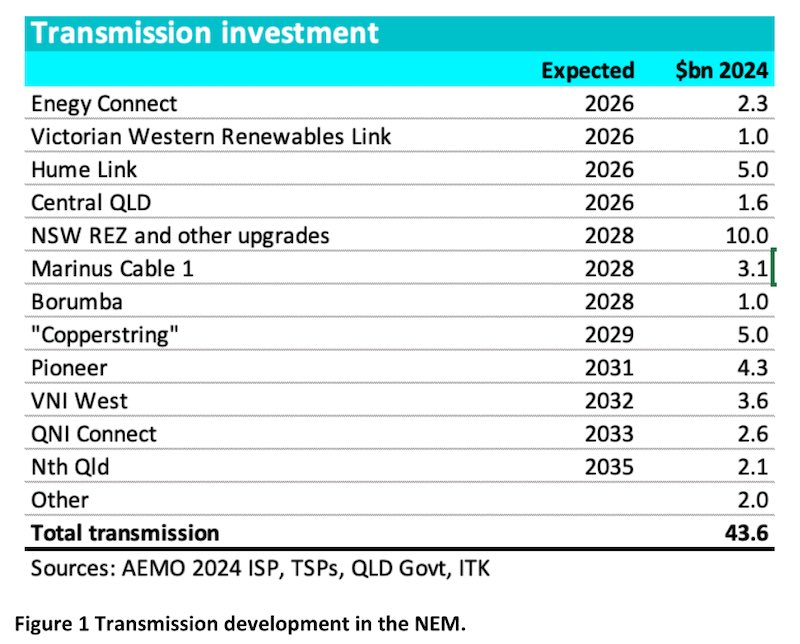

$40 billion of transmission under development, with $12 billion ready by 2028

There is over $40 billion of transmission under development.

But if I focus on NSW as the state with the highest forward prices and the largest consumer of electricity and look at when significant new transmission will be available I see:

Humelink, Orana will make a difference in NSW

In my opinion, Humelink is roughly on target to be built by December 2026. That’s despite ongoing opposition to building it above ground; despite not all easements being agreed, despite a recent 22km route length increase; and despite not one, but two upper house inquiries. And, despite the fact it has yet to get final approval from the AER or a final investment decision.

My confidence comes from the up to $600 million of pre-commitment spending that has already happened and will continue to take place ahead of the AER decision next year – and because the above-ground line is lower cost and faster to build than competing underground proposals.

Secondly, my guess is that the independent consortium developing the Orana REZ transmission link will be able to confirm that link in the near future. Confirmation of that should enable the pricing to be available to projects in that general area such as Liverpool Ranges Wind farm and Valley of the Winds wind farm.

Between those two projects alone and with the 800MW capacity of Project Interconnect now well underway NSW will have removed one of the many excuses that developers from Origin Energy to Tilt provide as to why they aren’t building projects.

Humelink could enable the south-west of NSW to leap ahead of the north

Few transmission lines can have been discussed as much as Humelink. Although some folk see it for better or worse as being built to facilitate Snowy 2, in my mind that is largely irrelevant.

Basically, I see Humelink as doing two main jobs. Firstly it’s basically the second half of the South Australia – NSW link (Project EnergyConnect); secondly it facilitates the increasingly attractive South West REZ.

Why is the Southwest REZ attractive? Well, basically, there are less people than in the north of state. One wind farm I looked at has only 32 affected residents. No people, no problem.

There are various large wind and solar farms planned for, say, the east of Balranald area that will have difficulty getting energy to NSW load without more capacity between Wagga and Sydney.

For example, the Yanco Delta project 10km north-west of Jerilderie (where I fly model planes every year and where Ned Kelly gave the bankers an early scare) is a 1.5GW wind project, quite well progressed in its EIS, that hopes to connect to Dinawan substation.

Dinawin is a substation built as a result of Project EnergyConnect, just to the west of Wagga. Equally, Spark Energy’s Dinawin Wind Farm is another 1500MW project at the scoping report stage. Dinawin is also where VNI West is scheduled to connect.

The 750MW Burrawong Wind Farm, close to Balranald, is a Windlab project at the SEARs stage.

The scoping report for Engie’s proposed 1800 MW “Plains Windfarm” near Hay has a map showing these developments. Engie is doing the job the NSW Department of Planning seems incapable of in providing a regional map.

Already the Wagga to Sydney transmission is so congested during the day that electricity flows almost every day but particularly in high solar days from higher priced NSW to lower or negatively priced Victoria (see What’s happening round Wagga).

Basically this entire precinct needs Humelink or something like it.