2023 has been declared as the year of the big battery in Australia, as approvals for wind and solar fell to eight year lows, and construction starts and project completions for new generation fell well below what is required for the country’s 2030 renewables target.

The Norway-based Rystad Energy has released its annual review for 2023, with the highlight being the record 3.7 gigawatts of construction starts for big battery projects across the country, some 50 per cent more than the combined construction starts of new wind and solar.

Battery storage will be important for Australia’s green energy transition, particularly as the share of renewables surges beyond 50 per cent towards the federal government’s 82 per cent renewable target for 2030.

However, that renewable energy target – integral for the broader emissions reduction goals – won’t be reached without a significant scale up in approvals, construction and completion rates.

“Key challenges for the year included getting utility wind and solar projects approved and commissioning sufficient capacity to keep up with Australia’s target of 82% renewables by 2030,” the Rystad report says.

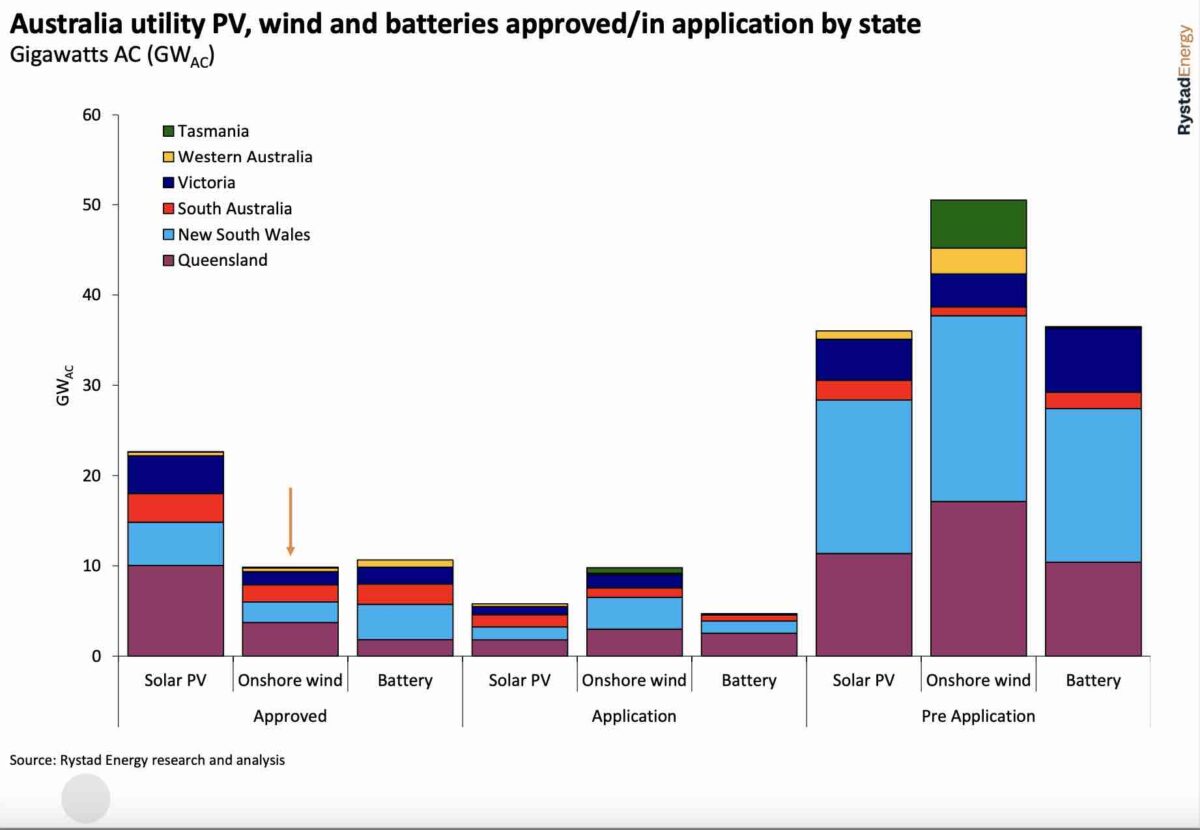

“A total of just 2.3 GWAC of utility solar and wind projects across Australia had their development application approved in 2023, the lowest in eight years. Just 4.6 GW of new wind and solar was energised in 2023, far below what is needed (more than 6 GW a year) to meet the 82 per cent target.”

According to Rystad, construction starts for new wind and solar projects also totalled just 2.3GW, with just 1 GW of new wind capacity, as the industry struggle increased turbine costs, a weakening Australian dollar and rising interest rates that pushed power purchase agreement prices above $100/MWh.

Only two wind assets broke ground in 2023: Tag Energy’s 756 MW first stage of the Golden Plains project in Victoria and Cubico’s 252 MW Wambo wind farm in Queensland.

It also noted the lack of approved wind projects across the NEM, with just 9 GW of wind power capacity approved but yet to start construction in the NEM.

Analysts say much more will be needed as most modellers suggest the grid needs more wind than solar over coming years. There is, however, more than 60GW of new wind capacity in the pipeline, waiting approvals or about to apply.

A total 1.3 GWAC of utility scale solar began construction in 2023, led by Acciona’s 380 MW Aldoga solar farm in Queensland, which accounted for most of the new construction starts. Rooftop solar continued its strong run with more than 3GW of new capacity.

The federal government has sought to unlock the deadlock in project development with a dramatic expansion of the Capacity Investment Scheme, which will now tender 9 GW of new storage capacity (average four hours) and 23 GW of new wind and solar capacity.

However, the details of the CIS, which will effectively use government funds to underwrite the risk of new projects by providing a floor and cap on project prices, have yet to be revealed, and the uncertainty is causing some potential PPA buyers to wait and see how the market unfolds.

Rystad estimates that the CIS will be successful in accelerating the rollout of wind and solar projects, but predicts the country could still fall short of its 2030 with just 70 per cent likely to be renewable – still a significant transition.

The good news, however, is in battery storage, which accounted for 60 per cent of new capacity construction starts in 2023.

These were led by landmark projects such as the Waratah Super battery (850MW and 1680 MWh), and the newly contracted Melbourne Renewable Energy Hub (600 MW and 1600 MWh), and the 500MW, 1000MWh first stage of the Eraring big battery.

Other notable battery project construction starts include Neoen’s Collie, Alinta’s Wagerup and Synergy’s Kwinana stage 2 projects in W.A., the Blyth battery in South Australia, the Tarong, Western Downs and Greenbank batteries in Queensland, and Latrobe and Rangebank batteries in Victoria.

Tesla was the most successful battery technology supplier, accounting for more than 1GW of new capacity (with various lengths of storage according to the individual projects needs), followed by the likes of Fluence, CATL, NHOA and Power Electronics.

In other technologies, Vestas accounted for the only two new wind projects, SMA and Ingeteam lead on solar farm inverters, and Nextracker and Array led on solar tracking systems, while JA Solar, Jinko, Canadian Solar, Longi, and Risen shared the spoils in solar modules.